Machine Learning-Driven and Statistical Algorithmic Trading for Cryptocurrency Markets

-

Supervisor Prof. Yiu Siu Ming Members Chu Tsun Hang 3036063747 Ma Tsz Hin 3036104242

Introduction

The cryptocurrency market’s constant operation and high volatility present significant risk management challenges that overwhelm traditional trading approaches. Static strategies become ineffective, making real-time, data-driven algorithmic programs essential for identifying and exploiting short-term opportunities. These machine learning models can process market nuances faster than humans, creating a competitive advantage by adapting to rapid changes.

Results

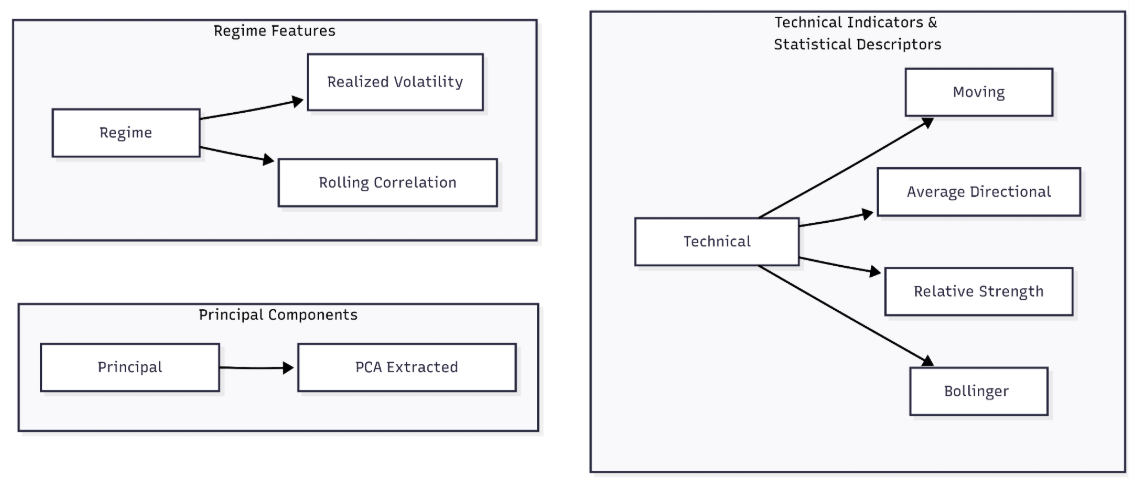

1. Data Pipeline and Feature Extraction

2. Backtest Performance

| Sharpe Ratio | Sortino Ratio | Calmar Ratio | Ann. Return | MDD | |

| Portfolio | 4.16 | 4.76 | 6.73 | 133.3% | -19.8% |

3. Real-trading Performance

| Portfolio/Fund | Returns | Drawdown | Sharpe Ratio |

| Project Portfolio(data from Exchange with trading fee included) | 23.70% | -5.12% | 2.03 |

| BarclayHedge Cryptocurrency Traders Index | -7.08% | NA | NA |

| Quant-Driven Multi-Factor Rota(data from Bybit without trading fee included) | -8.29% | -35.67% | -0.81 |

| COCI Quantum(data from Bybit without trading fee included) | -0.08% | -4.32% | -0.09 |

| Algo Intelligence Pro AI(data from Bybit without trading fee included) | -73.58% | -77.42% | -1.19 |